The Labyrinth of Underwriting: Navigating the Challenges in a Changing World

Related Articles

- Navigating The Choppy Waters: Job Market Uncertainty In The 21st Century

- The Geopolitical Tango: How Global Tensions Sway The Economy

- Unlocking The World Of Commercial Insurance Risks: A Comprehensive Guide For Business Owners

- Navigating The Pandemic’s Aftermath: A Deep Dive Into Insurance Claims

- Insurtech: The Future Of Insurance Is Here

Introduction

Join us as we explore The Labyrinth of Underwriting: Navigating the Challenges in a Changing World, packed with exciting updates

The Labyrinth of Underwriting: Navigating the Challenges in a Changing World

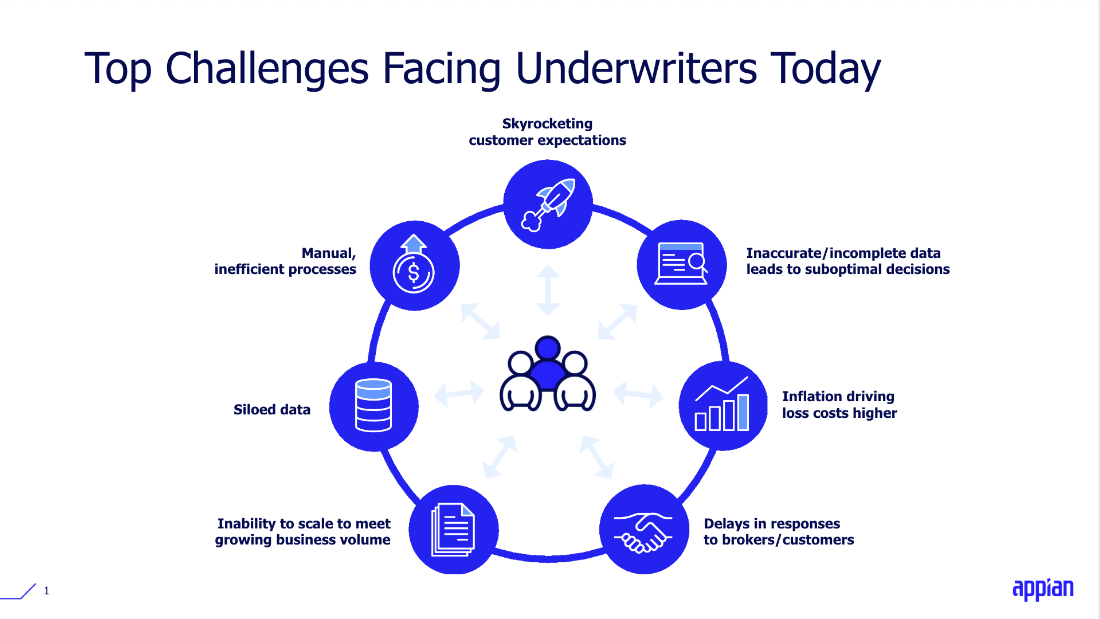

Insurance underwriting, the heart of the insurance industry, is a complex dance between risk assessment, data analysis, and human judgment. It’s about determining the likelihood of a claim, setting the right price, and ensuring the financial stability of the insurer. While the fundamentals remain constant, the underwriting landscape is constantly evolving, presenting a unique set of challenges for insurers today.

The Shifting Sands of Risk:

The world is becoming increasingly volatile. Climate change, technological advancements, and global events like pandemics are fundamentally altering risk profiles. This creates a significant challenge for underwriters who must adapt their models and assessments to account for these new realities.

- Climate Change and Natural Disasters: Rising sea levels, more frequent and intense hurricanes, and unpredictable weather patterns are driving up the cost of natural disaster claims. Underwriters need to assess the vulnerability of properties and adjust premiums accordingly. This requires sophisticated risk modeling tools and a deep understanding of climate science.

- Cybersecurity Threats: The digital landscape is rife with cyberattacks, from data breaches to ransomware. These incidents can result in significant financial losses for businesses and individuals, making cyber risk a major concern for underwriters. Determining the adequacy of cyber defenses and implementing appropriate coverage becomes critical.

- Emerging Technologies and Automation: The rise of autonomous vehicles, drones, and artificial intelligence is blurring the lines of traditional risk assessment. Underwriters need to understand the impact of these technologies on liability and risk profiles, developing new frameworks to evaluate them.

- The Pandemic’s Lasting Impact: The COVID-19 pandemic exposed vulnerabilities in supply chains, disrupted businesses, and forced a shift towards remote work. Underwriters need to consider the long-term implications of these changes on risk profiles, especially for businesses and individuals heavily reliant on specific industries.

Navigating the Data Deluge:

The availability of data is a double-edged sword for underwriters. While it offers unprecedented opportunities for risk assessment, it also creates challenges in managing and interpreting massive datasets.

- Data Overload: The sheer volume of data generated by businesses, individuals, and connected devices is overwhelming. Underwriters need efficient tools and algorithms to process and extract meaningful insights from this data deluge.

- Data Quality and Bias: The accuracy and completeness of data are crucial for effective risk assessment. Underwriters must address issues of data quality, including inconsistencies, missing information, and potential biases, to ensure reliable results.

- Data Privacy and Security: The increasing importance of data privacy regulations like GDPR and CCPA adds another layer of complexity. Underwriters need to balance the need for data with the responsibility to protect sensitive information, ensuring compliance with evolving privacy laws.

The Human Element: Bridging the Gap

While technology is transforming the underwriting landscape, the human element remains crucial. Underwriters need to balance the power of data with their own expertise and judgment.

- Understanding Context and Nuance: Data can provide valuable insights, but it cannot capture the full context of a risk. Underwriters need to use their experience and judgment to interpret data within the broader framework of individual circumstances and market trends.

- Building Relationships and Trust: Underwriting is not just about assessing risk; it’s also about building relationships with clients. Underwriters need strong communication skills to explain complex concepts clearly and build trust with policyholders.

- Adapting to Change and Continuous Learning: The insurance industry is constantly evolving. Underwriters need to be lifelong learners, staying up-to-date on new technologies, regulations, and risk trends to effectively adapt to the changing landscape.

The Future of Underwriting: Embracing Innovation

To navigate these challenges, insurers are embracing innovative solutions to enhance their underwriting processes.

- Artificial Intelligence and Machine Learning: AI and ML are being used to automate tasks, analyze vast datasets, and identify patterns that humans may miss. This can improve efficiency and accuracy in risk assessment.

- Predictive Analytics and Risk Modeling: Advanced analytics tools help underwriters predict future events, assess risk profiles more accurately, and develop tailored insurance products.

- Blockchain Technology: Blockchain can enhance transparency and security in data sharing and claims processing, reducing fraud and increasing trust in the insurance ecosystem.

- Data Visualization and User-Friendly Interfaces: Modern tools make it easier for underwriters to visualize complex data, gain insights quickly, and communicate their findings effectively.

FAQs

Q: What are the biggest challenges facing insurance underwriting today?

A: The biggest challenges include evolving risk profiles due to climate change, cybersecurity threats, emerging technologies, and the pandemic’s lasting impact. Additionally, managing and interpreting massive datasets while ensuring data quality and privacy is a significant hurdle.

Q: How is technology impacting underwriting?

A: Technology is transforming underwriting by automating tasks, improving risk assessment accuracy, and providing access to advanced analytics. AI, ML, predictive analytics, and blockchain are among the key technologies driving innovation.

Q: What skills are essential for successful underwriters in the future?

A: Successful underwriters in the future will need a strong understanding of data analytics, the ability to interpret complex data, and strong communication skills to build relationships with clients. They will also need to be adaptable and willing to embrace new technologies and evolving risk profiles.

Q: What are some of the trends shaping the future of underwriting?

A: Key trends include the increasing use of AI and ML, the development of more sophisticated risk models, and the adoption of blockchain technology. Insurers are also focusing on data visualization and user-friendly interfaces to make underwriting more efficient and accessible.

Conclusion:

The future of insurance underwriting is one of constant evolution and innovation. By embracing new technologies, adapting to changing risk profiles, and harnessing the power of data while maintaining the human element, insurers can navigate the challenges and build a more resilient and sustainable industry.

Source:

This article was written by an AI chatbot and does not have any specific sources. The information presented is based on general knowledge and research about insurance underwriting. For specific information and data, please consult reputable sources and industry experts.

Closure

We hope this article has helped you understand everything about The Labyrinth of Underwriting: Navigating the Challenges in a Changing World. Stay tuned for more updates!

Make sure to follow us for more exciting news and reviews.

Feel free to share your experience with The Labyrinth of Underwriting: Navigating the Challenges in a Changing World in the comment section.

Stay informed with our next updates on The Labyrinth of Underwriting: Navigating the Challenges in a Changing World and other exciting topics.