The Business Loan Credit Report: Your Company’s Financial Passport

Related Articles

- Business Liability Insurance: Your Safety Net Against The Unexpected

- Unlocking Growth: Your Guide To Business Loan Pre-Approval

- Navigating The Labyrinth: A Comprehensive Guide To Business Insurance Comparison

- Business Income Insurance: Protecting Your Bottom Line When The Unexpected Happens

- Accessing The Funding You Deserve: A Guide To Business Loans For Minority-Owned Businesses

Introduction

Welcome to our in-depth look at The Business Loan Credit Report: Your Company’s Financial Passport

The Business Loan Credit Report: Your Company’s Financial Passport

Imagine applying for a loan for your dream house. The bank would want to know your financial history, right? They’d check your credit score, see how you’ve managed your finances in the past, and use that information to decide if you’re a good risk.

It’s the same for businesses. When you apply for a business loan, lenders need to assess your company’s financial health. That’s where the business loan credit report comes in. It’s like a financial passport for your company, showcasing your creditworthiness to potential lenders.

What is a Business Loan Credit Report?

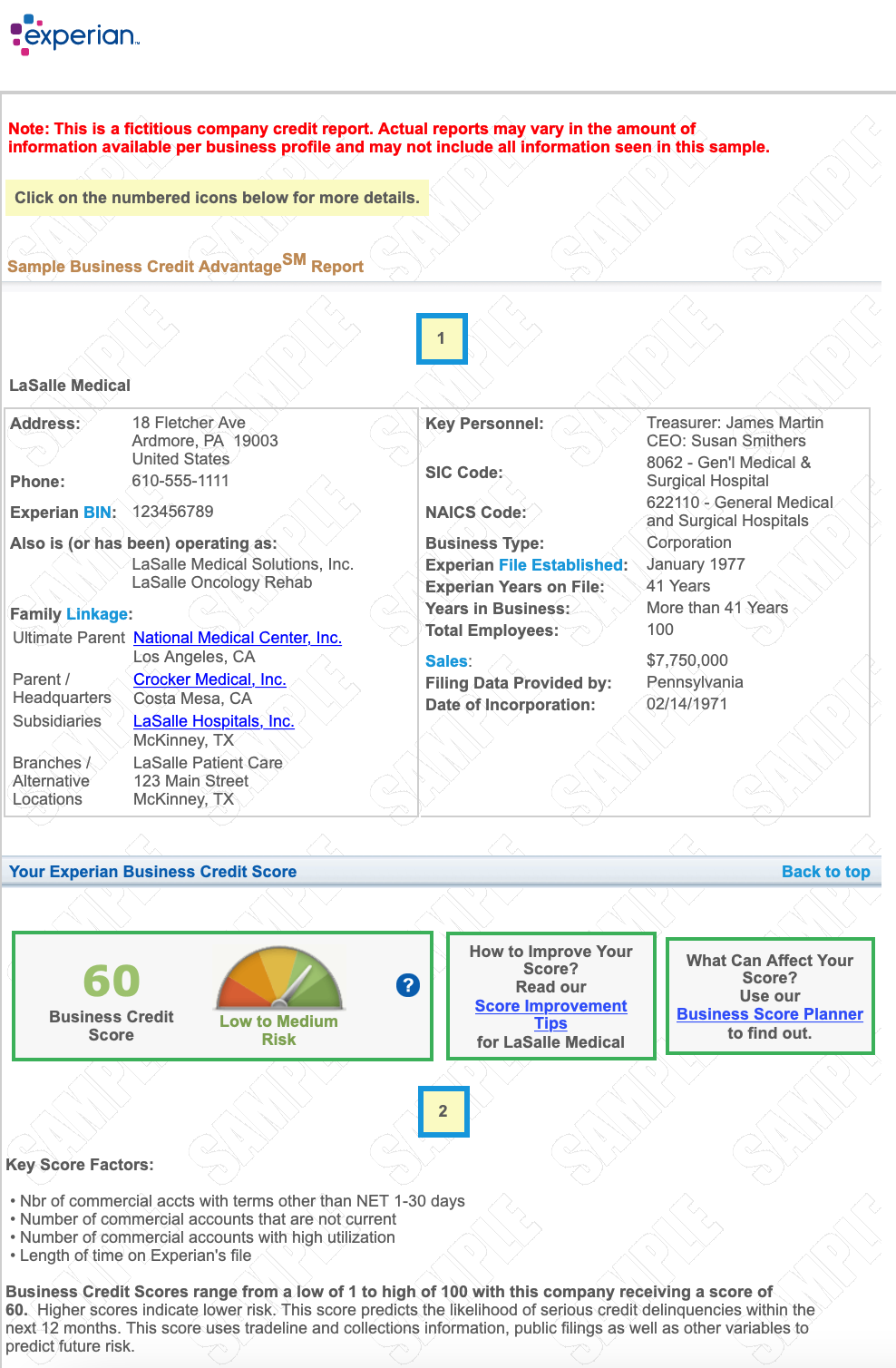

A business loan credit report is a detailed document that outlines your company’s financial history. It’s compiled by credit reporting agencies like Dun & Bradstreet (D&B), Experian, and Equifax, and provides lenders with valuable insights into your company’s creditworthiness.

Think of it as a comprehensive financial snapshot, encompassing:

- Payment history: This section shows your company’s track record of paying bills on time, including loans, utilities, and supplier invoices.

- Credit utilization: This reveals how much of your available credit you’re using. A high utilization ratio can signal financial strain.

- Public records: This includes information like bankruptcies, liens, and lawsuits that can impact your creditworthiness.

- Business information: Basic details about your company, including its legal structure, industry, and years in operation.

- Trade references: This section lists your company’s suppliers and how you’ve managed your accounts with them.

Why Do Lenders Need a Business Loan Credit Report?

Lenders use business loan credit reports to make informed lending decisions. Here’s why it’s crucial:

- Risk assessment: The report helps lenders assess the risk associated with lending to your business. A strong credit history indicates a lower risk, potentially leading to better loan terms and lower interest rates.

- Financial stability: Lenders use the report to gauge your company’s financial stability. A consistent history of timely payments and responsible credit utilization suggests a well-managed business.

- Predicting future performance: Past performance is often a good predictor of future behavior. A strong credit report indicates a track record of financial responsibility, which can increase the lender’s confidence in your ability to repay the loan.

How to Build a Strong Business Loan Credit Report

Building a strong business loan credit report is an ongoing process that requires careful attention to detail. Here’s how you can cultivate a positive credit profile:

- Establish Business Credit: Your first step is to establish business credit by obtaining a business credit card or line of credit. This helps build your credit history and allows credit reporting agencies to track your payment behavior.

- Pay Bills on Time: Punctuality is key. Pay all your bills, including loans, utilities, and suppliers, on or before the due date. Even a single late payment can negatively impact your credit score.

- Monitor Your Credit Report: Regularly review your business credit report for errors or discrepancies. You can access your reports for free from the major credit reporting agencies.

- Maintain Low Credit Utilization: Try to keep your credit utilization ratio low. A high utilization ratio can make your business appear financially strained.

- Establish Trade References: Develop strong relationships with suppliers and maintain a good payment history with them. These trade references can positively impact your credit report.

- Avoid Excessive Debt: Avoid taking on too much debt, as this can hurt your credit score. Focus on managing your existing debt responsibly.

- Be Mindful of Public Records: Be aware of any public records that could affect your credit report, such as lawsuits or bankruptcies.

Understanding Your Business Credit Score

Similar to personal credit scores, your business credit score is a numerical representation of your creditworthiness. It ranges from 0 to 100, with higher scores indicating better credit.

Here’s a general overview of business credit scores:

- Excellent: 80-100

- Good: 70-79

- Fair: 60-69

- Poor: 50-59

- Very Poor: 0-49

A higher business credit score can:

- Qualify for better loan terms: Lenders often offer lower interest rates and more favorable loan terms to businesses with strong credit scores.

- Secure financing more easily: Lenders are more likely to approve loan applications from businesses with good credit histories.

- Boost your company’s reputation: A strong credit score can enhance your company’s reputation and attract more customers and suppliers.

The Importance of Business Loan Credit Report Monitoring

Regularly monitoring your business loan credit report is crucial for maintaining a healthy financial profile. Here’s why:

- Detect errors: Errors can occur on credit reports, such as incorrect payment information or inaccurate account balances. These errors can negatively impact your credit score.

- Identify potential fraud: Monitoring your report can help you identify potential fraud, such as unauthorized credit accounts or fraudulent transactions.

- Stay informed: Regularly reviewing your report allows you to stay informed about your company’s financial health and identify any potential issues before they escalate.

How to Obtain Your Business Loan Credit Report

To obtain your business loan credit report, you can contact the major credit reporting agencies directly.

- Dun & Bradstreet (D&B): D&B is a leading provider of business credit information. You can access your D&B report through their website or by contacting their customer service.

- Experian: Experian offers a range of business credit reporting services, including credit monitoring and risk management solutions.

- Equifax: Equifax provides business credit reports and scores, along with data analysis tools to help businesses manage their credit.

Frequently Asked Questions (FAQs)

Q: What is the difference between a personal credit report and a business credit report?

A: A personal credit report tracks your individual financial history, while a business credit report focuses on your company’s financial performance.

Q: How long does it take to build a good business credit score?

A: Building a good business credit score takes time and consistent effort. It’s recommended to start establishing business credit as early as possible and maintain good financial practices over time.

Q: What happens if my business has a poor credit score?

A: A poor credit score can make it difficult to secure loans, lease equipment, or even obtain favorable terms from suppliers.

Q: Can I improve my business credit score if it’s low?

A: Yes, you can improve your business credit score by paying bills on time, managing your debt responsibly, and monitoring your credit report for errors.

Q: What are some tips for improving my business credit score?

A: Pay bills on time, keep credit utilization low, establish trade references, and monitor your credit report regularly.

Q: How often should I check my business credit report?

A: It’s recommended to check your business credit report at least annually, and more frequently if you’re applying for loans or other financing.

Q: What are the potential consequences of a bad business credit score?

A: A bad business credit score can lead to higher interest rates, limited access to financing, and even difficulty securing business partnerships.

Q: Can I dispute errors on my business credit report?

A: Yes, you can dispute errors on your business credit report by contacting the credit reporting agency directly.

Q: How can I get help building my business credit?

A: You can consult with a business credit expert or financial advisor for guidance on building and managing your business credit.

In conclusion, the business loan credit report is a vital document that reflects your company’s financial health. By understanding its importance and taking proactive steps to build a strong credit history, you can enhance your chances of securing financing, improve your business’s reputation, and unlock opportunities for growth.

References:

Closure

Thank you for reading! Stay with us for more insights on The Business Loan Credit Report: Your Company’s Financial Passport.

Don’t forget to check back for the latest news and updates on The Business Loan Credit Report: Your Company’s Financial Passport!

Feel free to share your experience with The Business Loan Credit Report: Your Company’s Financial Passport in the comment section.

Stay informed with our next updates on The Business Loan Credit Report: Your Company’s Financial Passport and other exciting topics.