Climate Change: A Growing Threat to the Insurance Industry

Related Articles

- When The Government Takes A Break: The Impact Of Shutdowns

- The Rising Tide: Understanding Insurance Claims Inflation And Its Impact

- Health Insurance Premiums: The Skyrocketing Costs And What You Can Do About It

- The Great Labor Shortage: Why Jobs Are Open And Workers Are Scarce

- The Looming Shadow: Risks Of A US Housing Market Crash

Introduction

In this article, we dive into Climate Change: A Growing Threat to the Insurance Industry, giving you a full overview of what’s to come

Climate Change: A Growing Threat to the Insurance Industry

The Earth’s climate is changing, and the effects are becoming increasingly apparent. From more frequent and intense heatwaves and wildfires to rising sea levels and devastating storms, the impacts of climate change are already being felt around the world. And the insurance industry, traditionally a pillar of stability and risk mitigation, is facing a growing challenge in adapting to this new reality.

A Shift in the Landscape:

The insurance industry is built on the principle of assessing and managing risks. For decades, these risks were largely predictable, based on historical data and established patterns. But climate change is disrupting this established order, introducing new and unpredictable risks that traditional models are struggling to accommodate.

The Rising Cost of Climate Change:

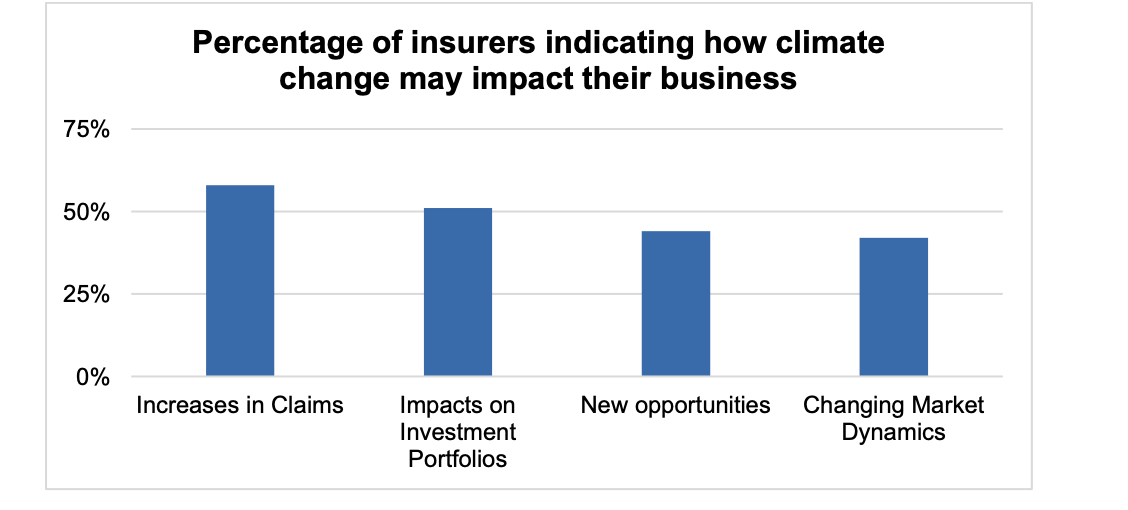

- Increased Claims: As extreme weather events become more frequent and severe, insurance companies are facing a surge in claims. From flooding and wildfires to hurricanes and hailstorms, the cost of damage is escalating rapidly.

- Higher Premiums: To offset the increased risk and rising claims, insurers are forced to raise premiums. This can create a vicious cycle, as higher premiums make insurance less affordable, potentially leading to a decline in coverage and leaving individuals and businesses more vulnerable to financial ruin.

- Underwriting Challenges: Predicting future risks becomes increasingly difficult in a changing climate. Traditional actuarial models, based on historical data, are no longer reliable in a world of unprecedented weather patterns. This uncertainty makes it challenging for insurers to accurately assess risks and set premiums, leading to potential underestimation and financial losses.

A Looming Crisis:

The insurance industry is facing a critical juncture. The changing climate poses a significant threat to its core business model. If insurers fail to adapt, they risk becoming insolvent, leaving policyholders without coverage and further exacerbating the financial burden of climate change.

The Need for Adaptation:

To navigate this challenging landscape, the insurance industry must embrace a proactive approach to adaptation. This involves:

- Improving Risk Assessment: Insurers need to develop new models and data analysis techniques that incorporate climate change projections and account for the evolving nature of risks.

- Developing Climate-Resilient Products: Innovative insurance products that address climate-related risks are crucial. This could include tailored coverage for specific climate hazards, climate-resilient building codes, and incentives for sustainable practices.

- Promoting Climate Action: Insurers can play a crucial role in promoting climate action by incentivizing sustainable practices, investing in renewable energy, and advocating for climate-friendly policies.

A Collaborative Effort:

Addressing the challenges posed by climate change requires a collaborative effort. Insurers need to work closely with governments, regulators, and other stakeholders to develop effective solutions. This could involve:

- Developing Climate-Resilient Infrastructure: Investing in infrastructure that is better equipped to withstand extreme weather events is essential to mitigate the impacts of climate change.

- Implementing Climate-Smart Policies: Governments need to implement policies that encourage climate-friendly practices, such as carbon pricing, renewable energy subsidies, and building codes that promote energy efficiency.

- Sharing Data and Expertise: Collaboration between insurers, researchers, and government agencies is crucial to improve risk assessment, develop innovative solutions, and promote climate action.

Beyond Financial Risks:

The impact of climate change extends beyond financial risks. The increasing frequency and severity of extreme weather events pose a threat to human life, infrastructure, and ecosystems. The insurance industry has a responsibility to contribute to the broader efforts to mitigate climate change and build a more resilient future.

The Future of Insurance:

Climate change is reshaping the insurance industry. The companies that adapt most effectively will be the ones that thrive. This will require a commitment to innovation, collaboration, and a deep understanding of the evolving risks posed by a changing climate.

FAQ:

Q: How is climate change impacting the insurance industry?

A: Climate change is leading to more frequent and intense extreme weather events, resulting in increased claims, higher premiums, and challenges in risk assessment for insurers.

Q: What can insurance companies do to adapt to climate change?

A: Insurers can adapt by improving risk assessment, developing climate-resilient products, promoting climate action, and collaborating with governments and other stakeholders.

Q: What are the potential consequences if the insurance industry fails to adapt?

A: If insurers fail to adapt, they risk becoming insolvent, leaving policyholders without coverage and exacerbating the financial burden of climate change.

Q: What role can the insurance industry play in mitigating climate change?

A: Insurers can play a role in mitigating climate change by incentivizing sustainable practices, investing in renewable energy, and advocating for climate-friendly policies.

Q: What are some examples of climate-resilient insurance products?

A: Examples include flood insurance, wildfire insurance, and insurance for renewable energy projects.

Q: What are some of the challenges facing the insurance industry in adapting to climate change?

A: Challenges include the difficulty of predicting future risks, the need for new data and models, and the potential for regulatory changes.

Q: What are some of the opportunities for the insurance industry in a changing climate?

A: Opportunities include developing new products and services, expanding into emerging markets, and playing a leadership role in climate action.

Q: What is the role of governments in addressing the challenges posed by climate change to the insurance industry?

A: Governments can play a role by implementing climate-smart policies, providing incentives for climate-resilient infrastructure, and promoting collaboration between insurers and other stakeholders.

References:

- Climate Change and the Insurance Industry: A Systemic Risk

- Climate Change and the Insurance Sector

- Insurance and Climate Change: A Growing Challenge

- The Insurance Industry and Climate Change

- Climate Change and the Insurance Industry: A Review of the Literature

Closure

Thank you for reading! Stay with us for more insights on Climate Change: A Growing Threat to the Insurance Industry.

Make sure to follow us for more exciting news and reviews.

Feel free to share your experience with Climate Change: A Growing Threat to the Insurance Industry in the comment section.

Stay informed with our next updates on Climate Change: A Growing Threat to the Insurance Industry and other exciting topics.