Term life insurance vs whole life

Related Articles

- America’s Economic Crossroads: Navigating The Path To Prosperity

- Navigating The Health Insurance Marketplace In 2024: Your Guide To Finding The Perfect Plan

- Unlocking Savings: A Comprehensive Guide To Reducing Your Health Insurance Costs

- Unlocking The World Of Commercial Insurance Risks: A Comprehensive Guide For Business Owners

- The Widening Gap: A Look At Income Inequality In The US

Introduction

Welcome to our in-depth look at Term life insurance vs whole life

Term vs. Whole Life Insurance: Which One is Right for You?

Life insurance is a crucial part of financial planning, especially if you have dependents. It provides a financial safety net for your loved ones in case of your untimely demise, ensuring their financial stability. But with a plethora of options available, choosing the right life insurance policy can feel overwhelming.

Two main types of life insurance dominate the market: Term Life Insurance and Whole Life Insurance. Both offer financial protection, but they operate differently, catering to distinct needs and financial goals. This guide will delve into the nuances of each policy, helping you understand which one best suits your circumstances.

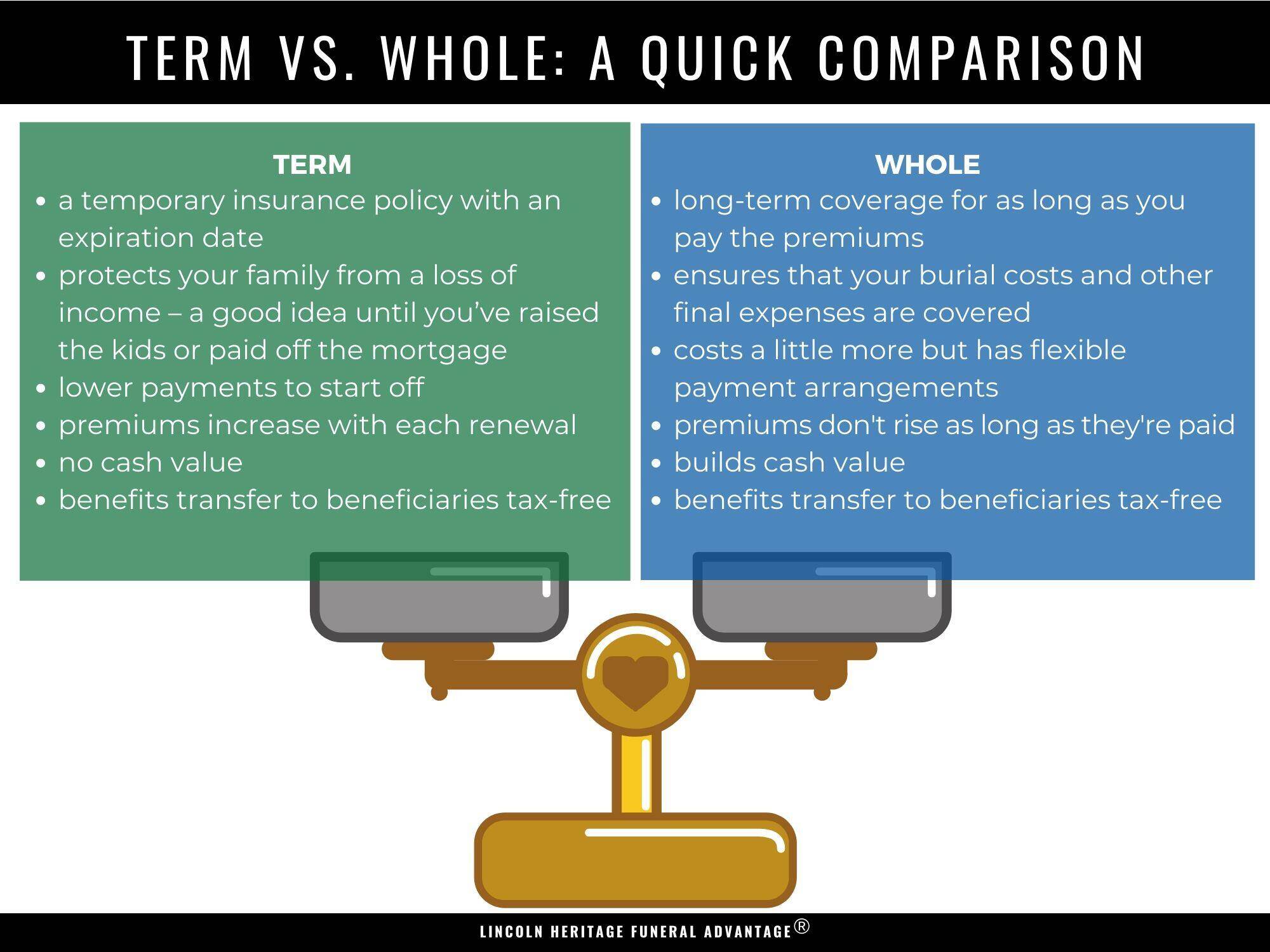

Term Life Insurance: The Foundation of Financial Security

Imagine building a house. You need a strong foundation to support the structure. Term life insurance serves as that foundation, providing a safety net for your loved ones during a specific period.

Here’s a breakdown of Term Life Insurance:

- Term: As the name suggests, term life insurance provides coverage for a fixed period, typically ranging from 10 to 30 years. This period aligns with specific life stages, like raising children or paying off a mortgage.

- Pure Protection: Term life insurance focuses solely on providing a death benefit. If you pass away during the policy term, your beneficiaries receive a predetermined lump sum payment.

- Affordable: Term life insurance is generally the most affordable option, offering significant coverage at a lower premium compared to whole life insurance.

- No Cash Value: Term life insurance doesn’t accumulate cash value. It’s a pure protection plan, with premiums dedicated solely to providing a death benefit.

- Renewability and Conversion: Most term life insurance policies offer the option to renew the policy at the end of the term, albeit at a higher premium due to your increased age. You can also convert your term life insurance policy to a permanent life insurance policy, like whole life, within a specified timeframe.

Who benefits from Term Life Insurance?

- Young families with mortgage and childcare expenses: Term life insurance provides a financial safety net for your family during their most vulnerable years.

- Individuals with short-term financial obligations: If you have a large debt, like a student loan or business loan, term life insurance can ensure your loved ones aren’t burdened with that debt in your absence.

- People on a tight budget: Term life insurance offers excellent value for money, providing substantial coverage at an affordable price.

Whole Life Insurance: A Lifetime of Security and Investment

Think of whole life insurance as a well-built house, offering long-term security and potential investment opportunities.

Here’s a deeper look at Whole Life Insurance:

- Permanent Coverage: Unlike term life insurance, whole life insurance provides lifelong coverage, ensuring your beneficiaries receive a death benefit regardless of when you pass away.

- Cash Value Accumulation: Whole life insurance policies build cash value over time. A portion of your premium goes towards this cash value, which you can access through withdrawals, loans, or even use it to pay your premiums.

- Investment Component: The cash value in whole life insurance policies is typically invested in a variety of financial instruments, potentially generating returns. However, the returns are often lower than other investment options.

- Higher Premiums: Whole life insurance premiums are typically higher than term life insurance premiums, reflecting the lifetime coverage and cash value accumulation features.

- Limited Flexibility: Whole life insurance policies offer limited flexibility compared to term life insurance. Changing your coverage or premiums can be challenging and might involve additional costs.

Who benefits from Whole Life Insurance?

- Individuals seeking lifelong coverage and a potential investment vehicle: If you want to ensure your family is financially secure for generations to come, whole life insurance can be a suitable option.

- People with a high net worth and a desire for estate planning: Whole life insurance can be a valuable tool for estate planning, offering tax advantages and wealth transfer strategies.

- Those looking for a guaranteed return on their investment: While the returns on whole life insurance are often modest, they offer a guaranteed minimum return, providing a sense of security.

The Term vs. Whole Life Insurance Showdown: Choosing the Right Fit

Choosing between term life insurance and whole life insurance depends on your individual needs, financial situation, and long-term goals.

Term Life Insurance is ideal for:

- Short-term financial protection: If you need coverage for a specific period, like raising children or paying off a mortgage, term life insurance offers affordable and effective protection.

- Budget-conscious individuals: Term life insurance is a cost-effective option, allowing you to maximize your coverage with minimal premium outlay.

- Individuals seeking flexibility: Term life insurance policies offer greater flexibility in terms of coverage adjustments and potential conversion to permanent life insurance.

Whole Life Insurance is suitable for:

- Long-term financial security: If you want lifelong coverage and a potential investment vehicle, whole life insurance provides a comprehensive solution.

- Individuals seeking a guaranteed return on their investment: Whole life insurance offers a guaranteed minimum return on your cash value, providing a sense of stability.

- High-net-worth individuals with estate planning needs: Whole life insurance can be a valuable tool for estate planning, offering tax advantages and wealth transfer strategies.

A Practical Approach to Choosing the Right Policy

Here’s a step-by-step approach to help you make the best decision:

- Assess your needs: Determine the purpose of your life insurance. Are you looking for short-term protection or lifelong coverage?

- Consider your financial situation: Evaluate your budget and determine how much premium you can comfortably afford.

- Explore different options: Get quotes from multiple insurance providers to compare premiums and coverage features.

- Seek professional advice: Consult with a financial advisor or insurance broker to discuss your specific needs and get personalized recommendations.

Beyond the Basics: Understanding Key Considerations

- Coverage Amount: Determine the appropriate coverage amount based on your dependents’ financial needs and your outstanding debts.

- Premium Payment Options: Explore different payment options, including monthly, quarterly, or annual premiums.

- Riders and Add-ons: Consider additional riders and add-ons that can enhance your coverage, such as accidental death benefit or critical illness coverage.

- Policy Transparency: Ensure you understand the policy terms and conditions, including exclusions, limitations, and renewal options.

FAQ: Your Life Insurance Queries Answered

Q: How much life insurance do I need?

A: There’s no one-size-fits-all answer. The ideal coverage amount depends on your dependents’ financial needs, your outstanding debts, and your lifestyle. A financial advisor can help you determine the right amount.

Q: Can I convert term life insurance to whole life insurance?

A: Yes, most term life insurance policies offer a conversion option within a specified timeframe. However, the conversion premium will be higher than the original term life insurance premium.

Q: Can I withdraw cash from my whole life insurance policy?

A: Yes, you can withdraw cash from your whole life insurance policy. However, withdrawals will reduce the death benefit and may impact the policy’s cash value accumulation.

Q: Is whole life insurance a good investment?

A: Whole life insurance offers a guaranteed return on your cash value, but the returns are often modest compared to other investment options. Consider your investment goals and risk tolerance before choosing whole life insurance.

Q: What happens if I miss a premium payment?

A: If you miss a premium payment, your policy may lapse. However, most insurance providers offer a grace period to make the payment. Contact your insurance provider immediately if you miss a payment.

Conclusion: Making the Right Choice for Your Future

Choosing between term life insurance and whole life insurance is a significant financial decision. By understanding the nuances of each policy, assessing your needs, and seeking professional advice, you can make the right choice for your family’s financial security.

Remember, life insurance is not just about protecting your loved ones financially, but also about providing peace of mind, knowing that their future is secure even in your absence.

Reference URL:

- https://www.investopedia.com/terms/t/termlifeinsurance.asp

- https://www.investopedia.com/terms/w/wholelifeinsurance.asp

- https://www.nerdwallet.com/articles/insurance/term-life-insurance-vs-whole-life-insurance

Closure

Thank you for reading! Stay with us for more insights on Term life insurance vs whole life.

Make sure to follow us for more exciting news and reviews.

We’d love to hear your thoughts about Term life insurance vs whole life—leave your comments below!

Stay informed with our next updates on Term life insurance vs whole life and other exciting topics.