Inflation: The Silent Threat to Your Life Insurance Coverage

Related Articles

- The Price Of Progress: Inflation, Wages, And The Growing Gap

- The Insurance Industry’s Digital Transformation: From Paper To Pixels And Beyond

- The Rollercoaster Ride: Understanding Small Business Insolvency Rates

- Navigating The Pandemic’s Aftermath: A Deep Dive Into Insurance Claims

- The Insurance Industry Is Facing A Tsunami Of Disruption: Are You Ready?

Introduction

Discover everything you need to know about Inflation: The Silent Threat to Your Life Insurance Coverage

Inflation: The Silent Threat to Your Life Insurance Coverage

Life insurance is a crucial financial safety net, designed to protect your loved ones from the financial burden of your passing. But what happens when the purchasing power of that safety net diminishes over time? This is where inflation comes into play, silently eroding the value of your life insurance coverage and potentially leaving your beneficiaries with less than they need.

Understanding the Impact of Inflation on Life Insurance

Inflation is the steady rise in the prices of goods and services over time. This means that the same amount of money buys less today than it did in the past. Imagine buying a loaf of bread for $1 in 1950. Today, that same loaf might cost $4. This difference in purchasing power is the essence of inflation.

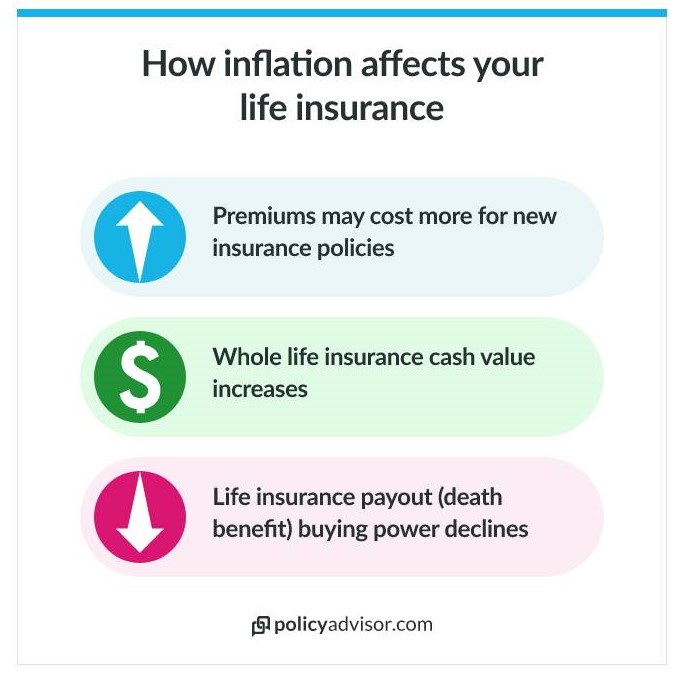

When it comes to life insurance, inflation has a significant impact on the value of your death benefit. Let’s say you bought a $1 million life insurance policy 20 years ago. While that might have seemed like a substantial amount at the time, inflation has likely eroded its purchasing power considerably. Your beneficiaries might receive $1 million today, but it might only have the buying power of $600,000 or less in today’s dollars. This means they could face a shortfall in funds to cover essential expenses like mortgage payments, education costs, and living expenses.

How Inflation Affects Life Insurance Policies

- Decreased Purchasing Power: The most significant impact of inflation is the diminished purchasing power of your death benefit. This means that while the face value of your policy remains the same, its real value decreases over time.

- Rising Costs: Inflation drives up the cost of living, making essential expenses like housing, healthcare, and education significantly more expensive. This makes it crucial for your beneficiaries to have enough money to cover these increasing costs.

- Investment Returns: Inflation can also impact the returns on your investments, which are often used to fund life insurance policies. If the rate of inflation outpaces your investment returns, you may need to adjust your policy or contribute more to maintain adequate coverage.

Strategies to Combat Inflation’s Impact on Life Insurance

Fortunately, there are several strategies you can employ to mitigate the effects of inflation on your life insurance coverage:

1. Regular Policy Reviews:

- Frequency: Review your policy at least every 3-5 years, or more frequently if you experience significant life changes like marriage, birth of a child, or a major career shift.

- Focus: Evaluate if your existing coverage is still sufficient to meet your family’s needs in today’s economic climate. Consider factors like rising housing costs, education expenses, and healthcare costs.

- Adjustments: If your current policy falls short, you might need to increase your coverage, adjust your beneficiary designations, or explore alternative life insurance products.

2. Consider Indexed Universal Life (IUL) Policies:

- Inflation Protection: IUL policies offer the potential for growth linked to a specific market index, such as the S&P 500. This can help offset the effects of inflation and potentially increase the death benefit over time.

- Flexibility: IUL policies provide flexibility in premium payments and death benefit options, allowing you to adjust your coverage as your needs and financial situation evolve.

- Potential for Growth: While not guaranteed, IUL policies have the potential for higher returns compared to traditional whole life policies, potentially outpacing inflation.

3. Adjust Your Beneficiary Designations:

- Review and Update: Regularly review and update your beneficiary designations to ensure they reflect your current financial situation and family dynamics.

- Consider Trusts: Setting up a trust for your beneficiaries can provide additional protection and ensure the funds are used responsibly, even if your beneficiaries are young or lack financial experience.

4. Invest in Additional Savings:

- Supplement Coverage: While life insurance provides a lump sum death benefit, additional savings can help your beneficiaries manage long-term financial needs.

- Diversify Investments: Diversify your investments across different asset classes, such as stocks, bonds, and real estate, to potentially mitigate the impact of inflation and generate consistent returns.

5. Seek Professional Financial Advice:

- Expert Guidance: Consult with a qualified financial advisor to discuss your specific financial situation and explore the best life insurance strategies to combat inflation.

- Personalized Solutions: A financial advisor can help you develop a comprehensive financial plan that includes life insurance, investment, and savings strategies tailored to your needs.

FAQ: Inflation and Life Insurance

Q: How do I know if my life insurance policy is sufficient to combat inflation?

A: A good rule of thumb is to aim for a death benefit that covers at least 10-15 times your annual income. However, this is just a starting point. Consider your family’s specific needs, including outstanding debts, housing costs, education expenses, and future financial goals. A financial advisor can help you determine the appropriate coverage amount.

Q: What if my policy doesn’t have inflation protection?

A: While many older policies don’t offer specific inflation protection, you can still take steps to mitigate its impact. Regularly review your policy, consider adjusting your beneficiary designations, and explore alternative life insurance products that may offer more protection against inflation.

Q: Are all life insurance policies affected by inflation?

A: Yes, all life insurance policies are affected by inflation to some extent. The purchasing power of your death benefit will decrease over time, regardless of the type of policy. However, some policies, like IULs, offer more protection against inflation than others.

Q: Can I adjust my existing policy to account for inflation?

A: Depending on your policy terms, you may be able to increase your coverage or adjust your premium payments to account for inflation. However, it’s essential to consult with your insurance provider or a financial advisor to understand your options and potential costs.

Conclusion

Inflation is an inevitable part of the economic landscape, and it’s crucial to understand its impact on your life insurance coverage. By proactively reviewing your policy, exploring alternative products, and seeking professional financial advice, you can ensure your life insurance continues to provide adequate protection for your loved ones, even in an inflationary environment. Remember, your life insurance is a vital financial safety net, and taking steps to combat inflation can help you maintain its value and protect your family’s financial well-being.

Source:

Closure

Thank you for reading! Stay with us for more insights on Inflation: The Silent Threat to Your Life Insurance Coverage.

Don’t forget to check back for the latest news and updates on Inflation: The Silent Threat to Your Life Insurance Coverage!

Feel free to share your experience with Inflation: The Silent Threat to Your Life Insurance Coverage in the comment section.

Stay informed with our next updates on Inflation: The Silent Threat to Your Life Insurance Coverage and other exciting topics.